Are Wealth Management Fees Tax Deductible? | Idaho Trust Bank

Published: 03/29/2024

By: Idaho Trust Bank

Wealth management* is a consultative service that provides clients with holistic financial guidance. Compared to standard asset management, which mainly revolves around investment advice, wealth management usually includes a wider range of financial services such as accounting, retirement planning, estate planning, and tax prep.

Working with an experienced advisor can help you make more valuable investments and better protect yourself against risk, but quality wealth management services can be costly. By understanding how financial advisory fees are assessed and taxed, you can identify new ways to reduce your annual expenses without sacrificing financial security.

What Are Financial Advisor Fees?

Wealth managers can charge you for their services in several different ways. The exact amount you’ll have to pay can vary based on the size of your account, your location, and your preferred approach to investment management.

Passive management, which mainly involves buying and holding long-term investments, typically has lower fees than active management, in which advisors actively select new stocks for your portfolio and track their performance in real-time.

The total size of your portfolio also plays a major role in determining your fee. Most advisors utilize a fee structure known as “assets under management,” or AUM. This means that the advisor collects a percentage of the money that they manage for each client, usually about 0.25% to 1% per year.

Advisors can also assess fees in other ways, such as by charging their clients a flat hourly rate for consultations or a separate pre-set fee for each service they receive (such as retirement planning or tax help). Regardless of the fee structure your advisor uses, the cost of wealth management services can quickly add up. As a result, many investors seek to deduct financial advisory fees from their yearly taxable income.

Are Financial Advisor Fees Tax Deductible?

Unfortunately, financial advisory fees are no longer tax deductible. Before 2018, investment-related expenses like financial advisory fees were legally deductible as miscellaneous itemized expenses. Under the old rules, individuals were allowed to deduct any investment-related expenses that exceeded 2% of their adjusted gross income (AGI) for the year.

However, most miscellaneous itemized deductions (including financial advisory fees) were eliminated as part of the 2017 Tax Cuts and Jobs Act. These changes are set to stay in effect through at least 2025, but miscellaneous itemized expense deductions could theoretically be reinstated after this period. Until this happens, investors must look for other ways to reduce their taxable income.

Tax Deductions for Investors

While financial advisory fees are no longer deductible, the tax code still includes several other notable deductions investors can use to save money. As an investor, it’s critical to understand these deductions and their rules, so you can safely and confidently take advantage of them.

401(k) Investment Plan

A 401(k) is a type of employer-sponsored retirement plan wherein employees defer a portion of their paychecks to their retirement accounts. Contributions to 401(k) plans are made on a pre-tax basis, which means the money you invest in your 401(k) will be excluded from your taxable income for that year.

There are specific IRS rules for 401(k) contributions that all taxpayers should be aware of. The maximum size for annual 401(k) contributions can change each year, generally increasing by a small amount due to cost-of-living adjustments.

Additionally, different types of 401(k) plans may have different restrictions on the amount of money that you can choose to defer into your account. If your plan has a lower limit, it reduces the amount that you can contribute each year. As an investor, you must carefully study the terms of your plan to determine the ideal contribution amount and maximize your tax savings.

Health Savings Account (HSA)

A Health Savings Account (HSA) is a type of savings account that allows you to defer money for qualified medical expenses on a pre-tax basis. Account holders can withdraw funds from their HSAs at any time, with no penalty or liability, as long as the money is used for qualified medical expenses.

The IRS defines qualified medical expenses as “expenses that would generally qualify for the medical and dental expenses deduction.” There are a wide variety of costs covered by a medical and dental expenses deduction, including doctors’ fees, hospital bills, prescription drug costs, health insurance premiums, and the cost of medical devices (such as mobility devices, false teeth, hearing aids, and prescription eyeglasses).

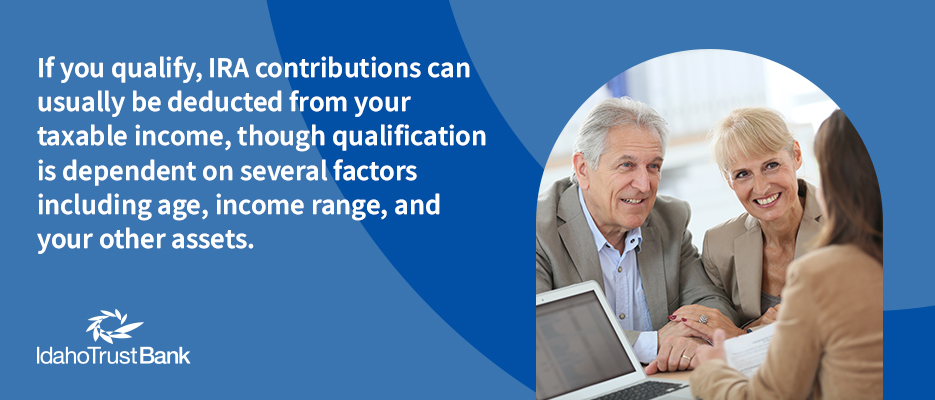

Individual Retirement Account (IRA) Contributions

Contributing to a traditional individual retirement account (IRA) is another way for individuals to save on their taxes while planning for the future. As opposed to 401(k) plans, which are employer-sponsored, traditional IRAs are established and managed by the account holder and their dependents.

If you qualify, IRA contributions can usually be deducted from your taxable income. The exact amount you can deduct depends on several factors, including your income range, your age, and your other assets. Individuals who already have employer-sponsored retirement plans may have smaller deduction limits on their IRA contributions than those with no other plan.

Investment Interest Expenses

Claiming interest expense deductions is another notable way for many investors to save on their taxes. Interest is the amount you must pay for the use of borrowed money. Generally, the interest expense deduction applies to purchases that are expected to increase in value or generate taxable investment income, such as real estate or shares of a particular business.

Individuals can claim deductions for the interest they pay on certain qualified expenses, including investments, mortgages, business expenses, and student loans. Personal interests, such as money paid toward car loans or credit cards, are not deductible.

While many investors are eligible for some interest expense deductions, the maximum amount you can deduct depends heavily on your income and the amount of interest you owe. Before claiming an interest expense deduction, it’s critical to obtain a thorough account of your assets, debts, and income.

Contact a local wealth management* expert!

At Idaho Trust Bank, we help clients create and preserve wealth for generations. Our local wealth management experts in Boise and Coeur d’Alene, Idaho, offer a personalized, relationship-based approach to wealth management services, retirement planning services, business succession planning, and trust and estate services. We will discuss your specific goals, risk tolerance, and current situation with you to create a LifeNeeds™ plan and set up a portfolio that works best for you. Contact one of our investment professionals today!

*NOT A DEPOSIT | NOT FDIC INSURED | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | NOT GUARANTEED BY THE BANK | MAY GO DOWN IN VALUE

The information provided herein is for general guidance only and should not be used as a substitute for consultation with professional tax, accounting, legal, or other competent advisers. Before making any decision or taking any action, you should consult a professional adviser who has been provided with all pertinent facts relevant to your particular situation. Tax articles on this website are not intended to be used and cannot be used by any taxpayer for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer.

Tax law is subject to continual change, and the information in this article is provided “as is,” with no assurance or guarantee of completeness, accuracy, or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability, and fitness for a particular purpose.